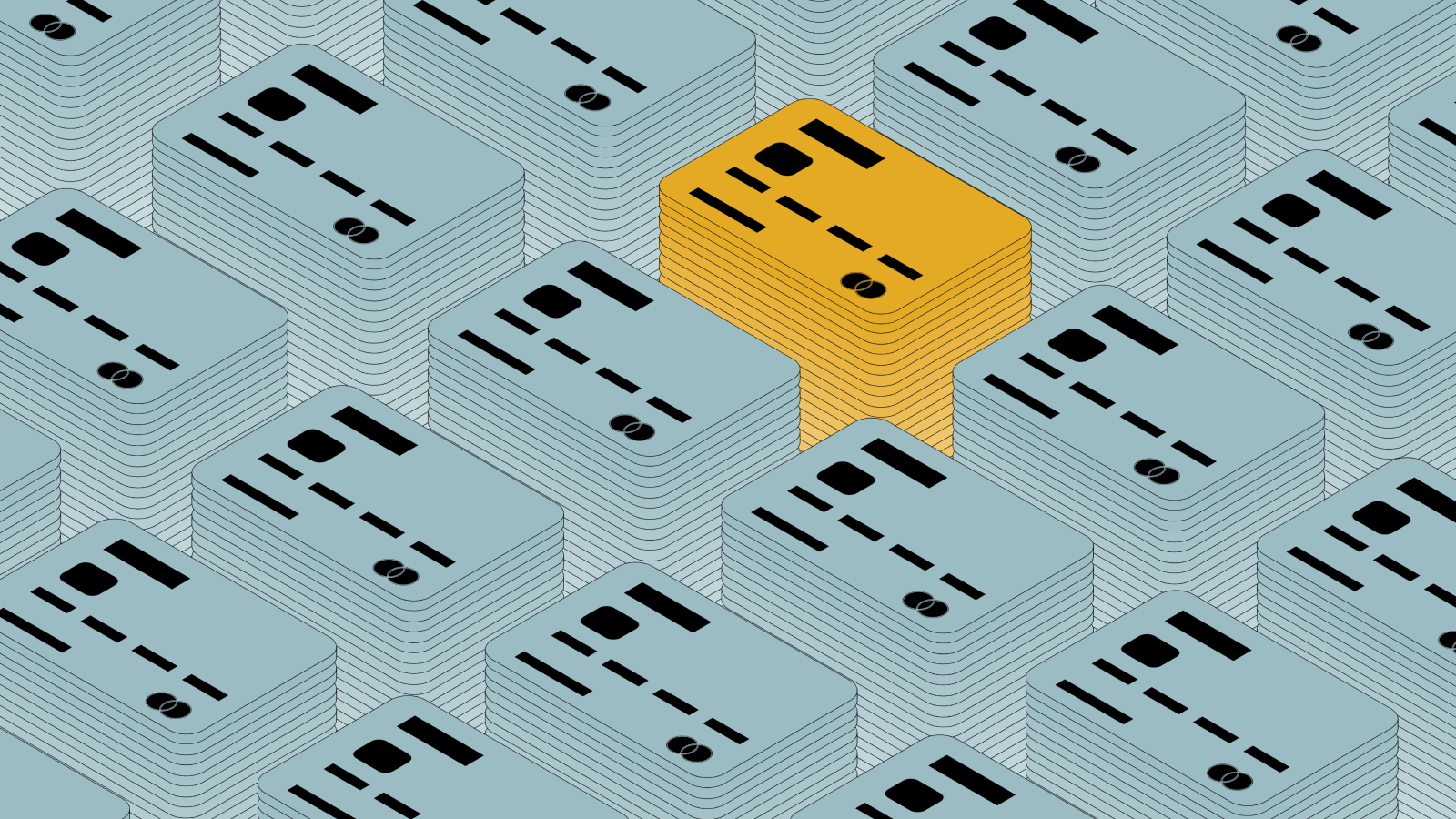

Credit cards as status symbols in society

For centuries, people have used luxury goods and property to signal their status in society. In the Middle Ages, European monarchs would demonstrate their wealth and power through huge palaces or rare jewels. Fast forward about 1,000 years and you’ll see people flaunting their wealth with sports cars, Gucci bags, or Rolex watches. This effect has been magnified exponentially with the advent of social media.

Individuals who can’t afford lavish items use more subtle and affordable indicators of prestige, like the newest iPhone model (not to say those don’t break the bank). Credit card companies have always understood this dynamic, and used branding brilliantly to benefit from it. Over time they have developed a system of tiered cards with labels like silver, gold, platinum, or black that symbolize special status, and set the premium cardholders apart from their lesser counterparts.

Another more recent invention is the metal credit card. Users love how heavy it feels in their hands, and the loud sound it makes when they slap it down on the counter to make a purchase. In addition, credit card companies use lounges, memberships, exclusive invites, and a host of other methods to help their top customers signal their societal status.

There are 42.7 million active credit cards in Canada.

A quick side note about credit card interest

The basics of credit card interest are actually very easy to grasp. You’re borrowing money from the credit card company and if you don’t pay it back when it’s due, you’re charged interest. Yet there are a few other things you’ll need to know if you really want to understand how credit card interest works.

Your credit score can have an impact on the interest rates available to you. As you improve your credit, you will have access to lower interest rates not just for credit cards, but for other forms of loans as well.

Your typical APR (Annual Percentage Rate) for most credit cards will be between 13.99% and 23.99%. It’s possible to find options that are below 10%, but that’s pretty rare. You’ll likely come across credit card offers with 0% APR, but be sure to look at the fine print as these are often introductory rates, and disappear after the first few months.

The average credit card interest in Canada is 19.99%

How you’re protected against credit card fraud

Credit cards protect you from purchase fraud on your card. If there is a purchase on your card that you did not authorize then you can let your credit card card company know and they will investigate. Essentially, you’re not responsible for losses that arise from situations that are not within your control.

When can you get a credit card?

Depending on the legal age of majority in your province or territory, 18 or 19-years-old is when you are allowed to sign up for a credit card. Starting credit history early is very beneficial, but if you're getting a credit card, make sure to practice responsible use, and don't get caught under a bunch of debt that could harm your credit in the future.

It used to be that people would most commonly use credit cards if they had plans for travelling, or expenses that needed to be made in the near future, like home renovations or vehicle repairs. Travel and rewards cards still encourage this type of use. These days there are many different types of credit cards that can be used to serve your needs. Let’s take a look at them now.

The 3 different types of personal credit cards

There are several types of credit cards that all serve different purposes or needs. Most fall within 4 main categories, and we’re going to dive in and explore the details, so you can make the best choice possible when you choose yours.

Standard credit cards

Standard credit cards are the most common type of credit card available. When people talk about “credit cards” they are usually referring to this type of card.

Let’s take a look at the pros and cons of standard credit cards.

Pros of standard credit cards:

- Most have better rewards programs and lower interest rates.

- You get the flexibility to make purchases online, or cover emergency costs.

- You can start (or continue) to build your credit score.

- Some cards offer certain insurance options (fraud, theft, travel).

Cons of standard credit cards:

- It can be more difficult to get approval if you have a lower credit score.

- If you don’t pay off your balance you incur debt.

- Some cards can come with high fees.

Standard credit cards don’t have many cons and that’s why people like them. If you don’t have the credit to get approved it’s not the end of the world. You can start with a secured card and build up your credit score.

Secured credit cards

A secured credit card is backed by a cash deposit that you have to make up front. This amount is going to be the same as your credit limit. Your deposit will be returned in full when you close the account, just as long as the card is in good standing.

Let’s take a look at the pros and cons of secured credit cards.

Pros of secured credit cards:

- Higher approval odds (usually guaranteed with a deposit).

- Great for building credit for those with low or no credit.

- Perfect for people who are anxious about credit card debt.

- Some secured cards still come with rewards.

Cons of secured credit cards:

- They often have higher interest rates than standard credit cards.

- Some have annual fees that can be costly.

- The rewards and benefits are less than with standard credit cards.

- It can be difficult to come up with the security deposit.

Secured cards aren’t supposed to be used forever. The purpose of a secured card is to build up your credit enough that you qualify for a standard credit card (one that doesn't require a deposit and has better benefits). When you are choosing a secured credit card, make sure you find one with little or no fees. Some secured cards only require a $50 security deposit to get started.

Prepaid cards

Prepaid cards are often mistaken for a credit card because they are powered by Mastercard or Visa. They are compared to secured cards, but function much differently. They are actually closer to a gift card than a credit card in that they don’t build your credit. However, you can make online purchases with them, which is quite handy.

Let’s take a look at the pros and cons of prepaid credit cards.

Pros of prepaid credit cards:

- They let you make Visa or Mastercard purchases like a real credit card.

- There are no interest charges.

- You can use them even if you are under the age of majority.

- Your credit history or score doesn’t matter for prepaid cards.

- There’s no application process, simply buy one from a store.

Cons of prepaid credit cards:

- No cashback or rewards.

- You can’t use them to build credit.

- Prepaid cards aren’t accepted everywhere.

- If you’re travelling, a card you bought in Canada might not work in the United States (be sure to read the terms and conditions).

- If your card is lost or stolen, the funds are not replaceable (it’s the same as losing cash).

There isn’t much more to say about prepaid cards. They make nice gifts, and are good if you’re in a pinch, but are really not credit cards in their truest form.

| Standard Card | Secured Card | Prepaid Cards | |

|---|---|---|---|

| Considered a Credit Card | ✅ | ✅ | 🚫 |

| Builds Credit | ✅ | ✅ | 🚫 |

| Guaranteed Approval | 🚫 | ✅ | N/A |

| Fraud Protection | ✅ | ✅ | 🚫 |

| Age of Majority Requirement | ✅ | ✅ | 🚫 |

| Incurs interest charges | ✅ | ✅ | 🚫 |

| Requires security deposit | 🚫 | ✅ | 🚫 |

| Requires credit application | ✅ | ✅ | 🚫 |

| Rewards programs | ✅ | ✅ | 🚫 |

| Acquired by purchasing | ✅ | 🚫 | ✅ |

Remember that prepaid cards are not actually credit cards, but we’ve included their information because they are often mistaken for them.

The 3 main credit card providers

Unless you've spent most of your life under a rock somewhere, or living in a monastery in Tibet, it’s likely you’ve heard of Visa, Mastercard, and American Express. That’s because these household names are the biggest players in the credit card game. What you may not know is that there are important differences between them you should know before you get a credit card. Here’s a rundown of each.

- Mastercard (over 266 million cards in circulation). No matter what you’re looking for, Mastercard is almost a must-have these days, as it is accepted worldwide. They provide large initial bonuses, attractive rewards, and low introductory interest rates.

- Visa (over 312.2 million cards in circulation). There is a reason that Visa is a household name, and there are a ton of great Visa cards out there today. It is the most widely accepted credit card network worldwide and has some of the best offers on the market, like big sign-up bonuses, 0% introductory APRs, rewards programs, and other money-saving features.

- American Express (over 48.4M cards in circulation). American Express (Amex) is the second largest credit card network in the United States by purchase volume. They typically target high-income individuals, and their products are tailored accordingly, which means they are great for people looking for lucrative rewards. However, they are not accepted as widely as Mastercard and Visa.

We’ll also want to cover rewards and how they tie in with the different “types” of credit cards. We’ve put together a little table to help you visualize the relationship between the two elements.

Final thoughts: focus on the benefits, not the flashy labels

Naming credit cards “platinum” and “gold” may have been an effective marketing device in the 90s, but this method has lost its shine, and consumers now want real value over flashy labels.

Some individuals don’t want to publicly display their personal financial status every time they make a purchase. Such blatant displays of wealth are sometimes considered to be a little tacky (unless you happen to be a famous musician or athlete, in which case, feel free).

Consumers want the option to have more features with their credit cards without making it obvious to everyone around them that they are comfortable financially. Conversely, if they are at a point in their lives where they can only afford basic credit cards, it should be their business and theirs alone. This means they look for a card that has the same branding regardless of the features that they subscribe to—one card for everyone.

If you really want to find a credit card that has the best value today, you need to look past the name on the card. To determine whether a credit card is really a good deal for you, review its rewards structures and interest rates, not its branding.

Let’s finish with a short list of things to look out for when choosing the right credit card for you:

- Do the rewards fit your spending habits? What will give you the most value?

- Is there an annual fee? Look for ones with no, or low annual fees!

- How high is the interest rate (this is more important if you're someone who tends to carry a balance.)

- Is there fraud, theft, or travel insurance?

- How’s the company's customer support? (You might want to head to Google for reviews from current cardholders.)

That’s all for this article. We hope you found the information we’ve provided to be helpful. Thanks for reading and good luck in your search for the perfect credit card!

Legal: This article provides information and is not intended to provide any personalized tax, investment, financial, or legal advice. You are encouraged to seek professional advice before making financial decisions.